JLL identifies the four districts with the highest investment potential for neighbourhood malls

Local malls are an attractive long-term investment with their resistance to tourist fluctuations and economic downturns

HONG KONG, 24 June 2019 – JLL identified that neighbourhood shopping malls in Cheung Sha Wan/Sham Shui Po, Tuen Mun, Shatin and Tseung Kwan O have the highest investment potential among the districts, according to its “Community Retailing – Uncovering the value of Hong Kong’s neighbourhood malls” research report released today.

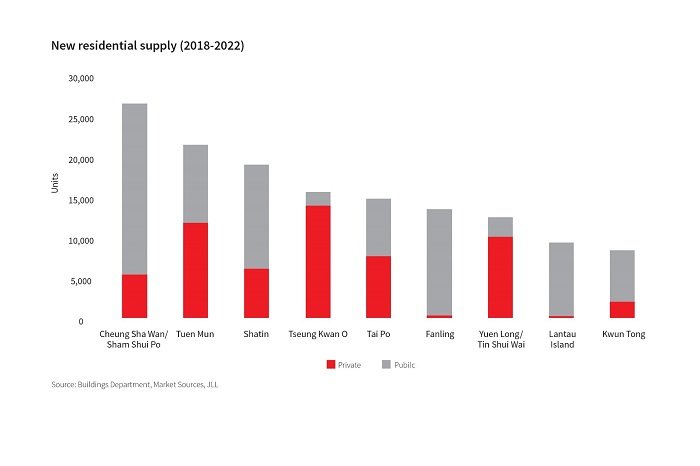

With neighbourhood malls typically capitalising on the everyday spending of nearby residents, an increase in population will result in expansion of the targeted catchment and translate into higher retail sales. Figures from JLL show Cheung Sha Wan/Sham Shui Po, Tuen Mun and Shatin will experience the most new residential supply between 2018 and 2022, which should translate to increased retail demand in those areas. It is estimated that the population of Cheung Sha Wan/Sham Shui Po will increase by just over 70,000 people by the end of 2022. JLL estimated that the new households that move to Cheung Sha Wan/Sham Shui Po could spend an additional HKD 180 million per month on non-discretionary items, with a large amount being spent in the area.

Another factor to consider is the types of households that move into an area. According to the Census and Statistics Department, the average expenditure on non-discretionary items for a household in private housing is 40% higher than that for a household in public housing. Therefore, neighbourhood malls in areas with a high proportion of new private housing supply such as Tseung Kwan O could benefit from new residents who have a higher propensity to spend. About 89% of the new housing supply in Tseung Kwan O will be private housing between 2018 and 2022.

JLL estimates there will be around 1.8 million sq ft of new neightbourhood mall supply between 2018 and 2022 across Hong Kong. It will provide investment opportunities to investors.

Investors have shown increasing interest in neighbourhood malls in recent years, pouring more than HKD 63 billion into the segment over the past decade. In 2009, neighbourhood malls attracted just over 8% of total investment in the city’s retail sector. In 2018, this had ballooned to 63% of total investment. Buyers include local investors, global and regional private equity as well as sovereign wealth funds.

“Neighbourhood malls in Hong Kong are an attractive retail asset worth considering for long-term investment due to stability, increased reliance on domestic consumers and relatively higher yields compared to other real estate classes. The strength of Hong Kong’s labour market and its growing population should continue to support these smaller localised malls.” said Denis Ma, Head of Research at JLL.

He said neighbourhood malls typically provide a yield premium over other real estate asset classes, which is attractive to investors. JLL estimates that as at the end of 2018, market yields for neighbourhood malls ranged between 3% to 4.5%, which is well above the city’s high street shops (2.5%) and Grade A offices (2.7%).

While retail trading conditions in Hong Kong tend to correlate strongly with inbound tourist arrivals, neighbourhood malls are a retail asset type that is more reliant on spending from Hong Kong residents, which has been far more stable than tourist spending. The strength of the Hong Kong economy has been a major factor, with the unemployment rate hitting a 20-year low of 2.8% in 2018. Wages have also increased steadily throughout this period, with disposable incomes growing at an average of 3.7% per year over the past decade, well above many other developed countries. Against this backdrop, domestic spending has been far less volatile. This is one of the major reasons why investors remain keen on neighbourhood malls as landlords can be confident that their tenants can withstand fluctuations in the inbound tourism market.

“About 76% of the tenants at neighbourhood malls are non-discretionary retail spending such as supermarkets, food and beverage operators and services, compared to 32% in premium shopping malls. These retail sub-sectors have been fairly resilient during tough economic conditions, which make neighbourhood malls a resilient investment class during an economic downturn. For example, back in 2009 following the global financial crisis, retail sales in supermarkets grew by 3.4% for the year, a strong performance compared with discretionary categories such as clothing and footwear, which declined by 0.8%,” he added.

About JLL

JLL (NYSE: JLL) is a leading professional services firm that specializes in real estate and investment management. Our vision is to reimagine the world of real estate, creating rewarding opportunities and amazing spaces where people can achieve their ambitions. In doing so, we will build a better tomorrow for our clients, our people and our communities. JLL is a Fortune 500 company with annual revenue of $16.3 billion, operations in over 80 countries and a global workforce of over 91,000 as of March 31, 2019. JLL is the brand name, and a registered trademark, of Jones Lang LaSalle Incorporated. For further information, visit jll.com.