COVID-19 and the China Office Market

Building a foundation for a stronger future in challenging times

China’s government is aggressively responding to the COVID-19 outbreak. Policies to support vulnerable SMEs have formed a protective barrier around much of the economy. Central authorities implemented fee reductions, liquidity injections, and the deferment of employee costs as early as January, representing a much more comprehensive response compared to the SARS outbreak in 2003. Moreover, the People’s Bank of China (PBOC) has announced its own measures to ease monetary pressure, adding to swift actions that are offsetting many of the outbreak’s short-term impacts. In turn, the government’s actions also have wide implications for the real estate market. The outbreak and policy response together are setting the unique stage for transformation in the office sector with risks and also potentials, forcing industry players to adapt in ways with wide implications and opportunities for the market going forward.

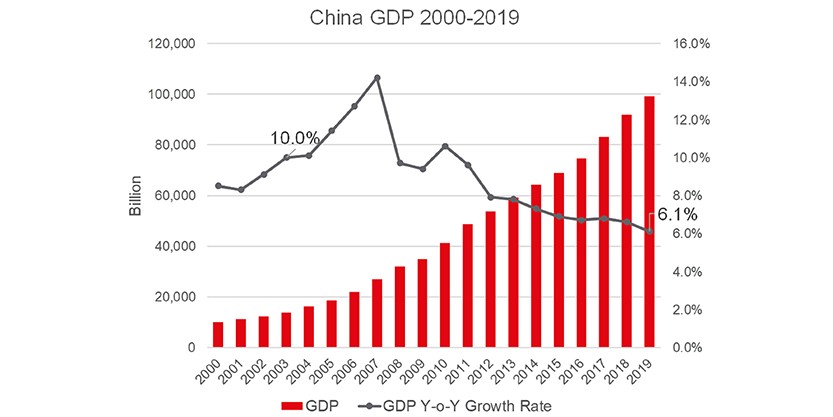

Figure 1

Robust policy measures are necessary because COVID-19’s domestic impact and global spread are likely to pose an even greater challenge for China than the one SARS presented in 2003. China at the onset of SARS was in the midst of an aggressive growth period. As Figure 1 shows, the SARS outbreak had little impact on China’s GDP growth in 2003, barely interrupting the economy’s steep upward trajectory. By contrast, in recent years China’s economy has become more mature and grown at more sustainable – but slower – rates. Rather than stoking an aggressive recovery like that seen after SARS, the current policy response likely will be focused on boosting the economy back to its recent pre-crisis growth trajectory.

For the office sector in particular, demand will see sharp impacts over the short-term. Tenants in industries requiring high degrees of person-to-person contact, such as travel and retail firms, will be the most affected by COVID-19. Additionally, production and supply chain disruptions are likely to cause manufacturers and trading companies to reduce their office leasing demand. This will further enhance the downward pressure on China’s office market. Nearly all cities have adjusted their 2020 office rental expectations downward in light of the outbreak.

While office market players should be clear-eyed about the difficult time ahead, it is also important to look at the potential for some positive outcomes and long-term outlook. There are still tenants and industries that are proving resilient to – or even thriving despite – the viral outbreak. Sectors that provide necessary services during times of crisis, including healthcare and insurance providers as well as online entertainment sectors, will provide some office leasing demand in the immediate term. Moreover, we expect demand from these sources to continue expanding once the outbreak recedes and policy stimulus lays the groundwork for recovery.

Insurance and healthcare sectors, unsurprisingly, continue to perform exceptionally well in 2020. The current government push to accelerate the development of new regulatory systems and accounting standards in the insurance industry are expected usher in a new period of development. Accordingly, insurers will likely upgrade office space and purchase properties for their own use as their needs expand. Another bright point is the TMT sector, especially the mobile gaming industry, which has grown rapidly with a compound annual growth rate of 24% in the past 5 years. As with the healthcare industry, the current epidemic has brought new development momentum to online entertainment, and it is expected that a portion of people who took up gaming during the outbreak will maintain their gaming habits after the epidemic is over.

Although the outbreak and containment measures stalled economic activity for an extended period, it is worth noting that while some business has been lost, perhaps more business was merely delayed, or pent-up. It is therefore imperative for all corporates to thoroughly review what opportunities have been lost, versus those that have only been pushed back. The firms that succeed will be those that focus on what activities can be made up in the remainder of the year, and not dwell on what may not return. Corporates that position themselves to benefit from a pent-up release of economic activity after the outbreak may able to move forward with leasing plans faster than they currently anticipate.

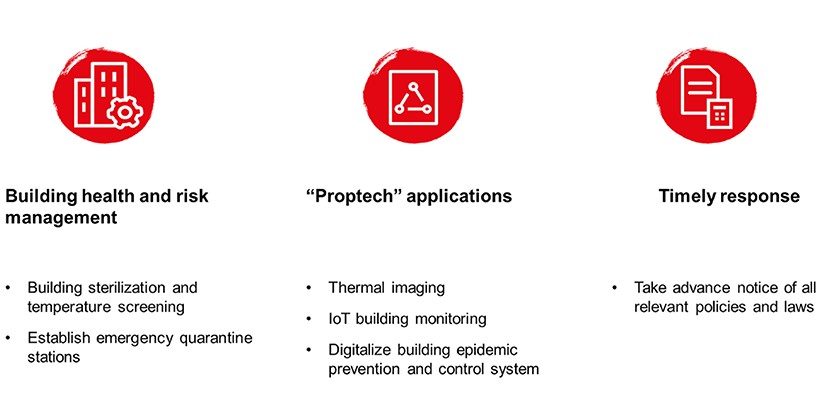

The COVID-19 outbreak also has notable implications for landlords (see Figure 3). Tenants are likely to desire more flexible accommodation patterns, given the interruption in business activities. Rental reduction policies, in a situation where both tenants and landlords face cost-related pressures, provide a win-win solution that may enhance long-term cooperation and generate goodwill between the two parties.

The outbreak has led landlords to build greater familiarity with prop-tech solutions, as new government mandates require implementation of updated specifications. Landlords have accelerated the development of health-related solutions for building management, including thermal imaging cameras and digital building control systems. These new features will remain in place after the outbreak has abated. Meanwhile tenants have shown interest in even low-tech responses to the outbreak, such as healthcare stations with hand sanitizer, public area sterilization protocols, controlled access gates, automatic elevators, and improved ventilation.

Figure 2

For occupiers, remote working arrangements are expected to be more widely applied and optimized. Many companies already are implementing strategies and technologies to enable effective workflow from outside the office, including replacing face-to-face meetings with conference and video calls, limiting the flow of employees through the office, and cancelling non-essential travel. We expect greater investment in technologies that enable non-physical access to resources, such as networked hard drives, cloud applications, and online (or mobile app-enabled) employee management software.

Looking ahead, tenant familiarity with these solutions may encourage occupier interest in flexible space over the long term as companies embrace enhanced connectivity and flexibility. As we have seen with the increased implementation of flexible space in traditional office blocks, this segment of the office leasing sector is already gaining traction, and the outbreak may very well help to boost if further.

Outlook

In the near-to-mid-term, measures to control construction will likely cause a large part of 2020 office supply to delay to 2021, and we expect that government stimulus policies will continue to support the economy in the near-term as COVID-19 is being contained. Looking further ahead, long-term demand drivers will still hinge on continued financial and market reform, innovation, and technological progress.

Emerging industries are expected to serve as a new engine for growth in China’s Grade A office market. Most notably, the government continues to accelerate the opening of the financial services industry to foreign players. In terms of technology and innovation, the digital economy could maintain an average annual growth rate of 10-15% moving forward. This likely would translate into growth for the TMT industry, with additional increases in investment and office demand as traditional industries continue to digitalize their services. Meanwhile, regional development initiatives mean we are seeing accelerated development in city clusters such as the Greater Bay Area, Beijing-Tianjin-Hebei, Yangtze River Delta, and Chengdu-Chongqing. In the future, the authorities will continue allocating resources to build up these areas as key nodes of China’s economy.

In both its impact within China as well as its global spread, COVID-19 is likely to test the market to an even greater extent than SARS in 2003. However, China’s combination of effective policymaking, expanding demand from dynamic sectors, agile responses from landlords and tenants, and strong long-term fundamentals demonstrate the market’s capacity to adapt to changing circumstances. Many of the economic downsides of this outbreak are being effectively mitigated, while positive ramifications, including increased attention to wellness-related office standards and flexible working environments, can be expected to resonate well after the current outbreak recedes.